Investors have had a jittery August so far. The ongoing (never-ending?) US/China trade spat continues to lurch along with no resolution in sight, a potential “hard Brexit” looms in the UK, and EU powerhouse Germany is teetering on the edge of recession. These concerns helped drive a 6% pullback in the S&P 500 between the end of July and mid-August, accompanied by a rush of capital into so-called “safe havens” like government bonds.

Investors have had a jittery August so far. The ongoing (never-ending?) US/China trade spat continues to lurch along with no resolution in sight, a potential “hard Brexit” looms in the UK, and EU powerhouse Germany is teetering on the edge of recession. These concerns helped drive a 6% pullback in the S&P 500 between the end of July and mid-August, accompanied by a rush of capital into so-called “safe havens” like government bonds.

In fact, the global appetite for safety at any cost has created a bizarre and unprecedented situation in which investors are willing to pay for the privilege of lending money to governments and high-quality corporations. In other words, frazzled investors are willing to buy bonds with negative yields, which guarantees that they will lose (a small amount of) money if they hold those bonds through maturity. This is a very high price indeed to pay for the perception of safety. The upshot is that there are currently more than $16 trillion of bonds outstanding with negative yields.

Although U.S. government bond yields are not (yet) negative, 10-year Treasuries yield less than half what they did last November. At 1.56%, the yield on the benchmark Treasury is now within striking distance of the all-time low of 1.35% set in July 2016. We find these puny yields to be deeply unappetizing for long-term investors. Consider that an investor in a 10-year Treasury today will pay 64x times “earnings” for an asset that is guaranteed to deliver zero capital appreciation if held until maturity.

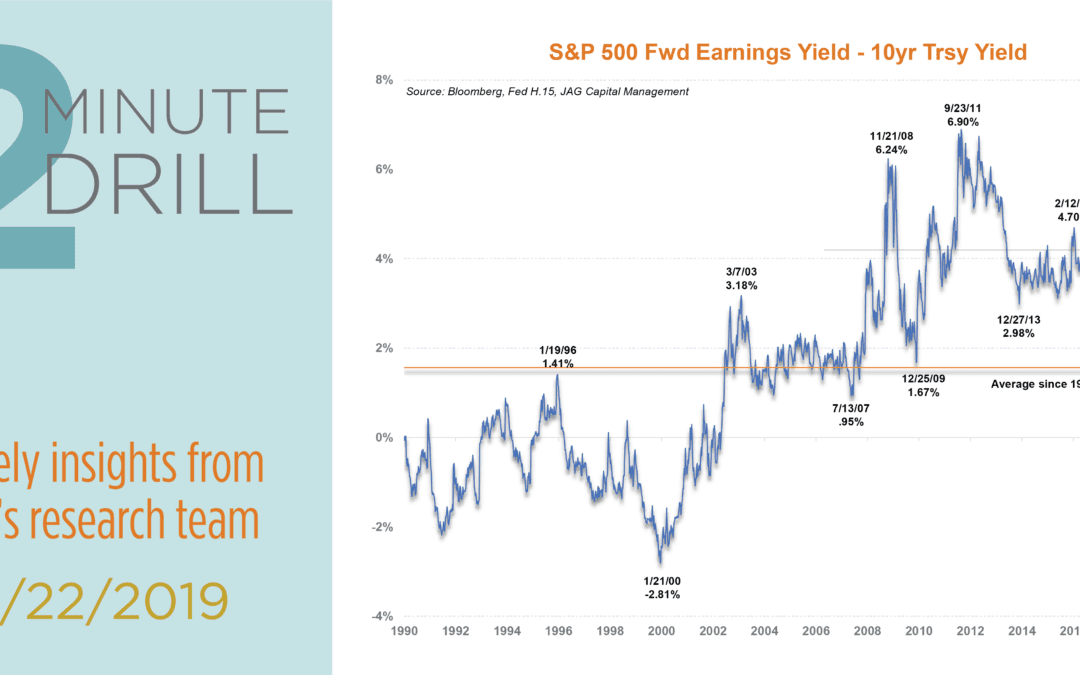

If long-term bonds appear to be overvalued, how should investors appraise stock market valuations? One way to make a reasonable stock-to-bond comparison is to examine earnings yields – which are the inverse of the more-commonly used P/E ratio. As these charts detail, the S&P 500 is currently cheaper on a forward earnings yield basis than it has been in years. This holds true when we compare stocks to both Treasuries and BAA-rated corporate bonds. Does this mean that stocks are certain to outperform bonds over the coming months? Of course not. For example, a deep recession within the next 12-18 months could greatly depress corporate earnings. And general stock market volatility makes predicting short-term market movements a fool’s errand. But for investors with 5-10-year time horizons and longer, we believe equities are highly likely to generate better inflation-adjusted returns than long-term bonds.

If long-term bonds appear to be overvalued, how should investors appraise stock market valuations? One way to make a reasonable stock-to-bond comparison is to examine earnings yields – which are the inverse of the more-commonly used P/E ratio. As these charts detail, the S&P 500 is currently cheaper on a forward earnings yield basis than it has been in years. This holds true when we compare stocks to both Treasuries and BAA-rated corporate bonds. Does this mean that stocks are certain to outperform bonds over the coming months? Of course not. For example, a deep recession within the next 12-18 months could greatly depress corporate earnings. And general stock market volatility makes predicting short-term market movements a fool’s errand. But for investors with 5-10-year time horizons and longer, we believe equities are highly likely to generate better inflation-adjusted returns than long-term bonds.