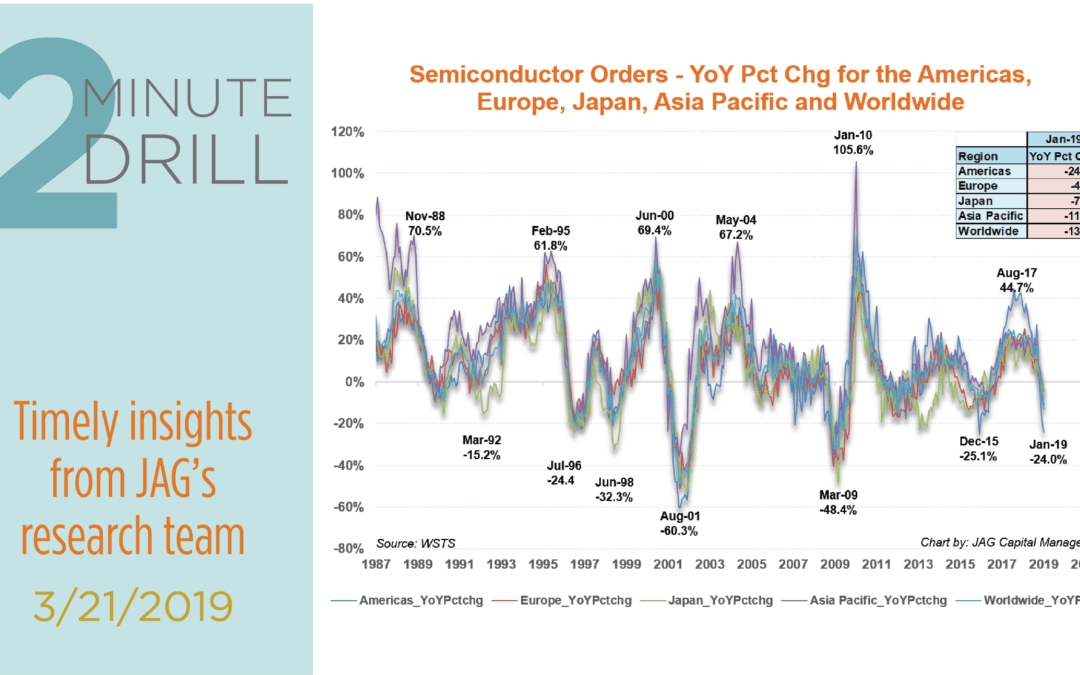

Semiconductor chips are essential to modern life, as they are the “brains” that power everything from smartphones to iPads to cars, communication networks, and household appliances. However, despite their importance to the global economy, the cyclicality of the semiconductor industry can make it challenging for investors to navigate. As this chart shows, global semiconductor orders are highly volatile, oscillating between multi-year peaks and troughs. The most recent peak in semiconductor orders occurred in August 2017, when they were up 44.7% year-over-year. Since then, orders have been trending down, to a recent -24% year-over-year decline as of January 2019. In fact, this has been one of the worst yearly order declines outside of recessions since 1987. We think orders are nearing a trough – and judging by the information we have gleaned from a wide variety of recent industry earnings calls, corporate management teams seem to agree. Many are calling for semiconductor industry conditions to improve within the next 1-2 quarters. In previous cycles, investors have been much better served to invest when orders are troughing rather than when they are peaking. Following the last 2009 and 2015 troughs in global orders, the S&P 1500 Semiconductor Equipment Index posted average yearly gains of more than 40%. Investors who invested at the 2010 and 2017 peaks in orders did not fare anywhere near as well. Although the Semiconductor Equipment Index managed to gain 37.7% in the year following the 2010 peak in orders, the Index managed only a 5.9% gain in the year after the August 2017 top in orders. We have an increasingly positive view toward semiconductor companies. We see valuations as undemanding, and the potential for orders firming into summer 2019 could create significant upside for investors over the coming year.