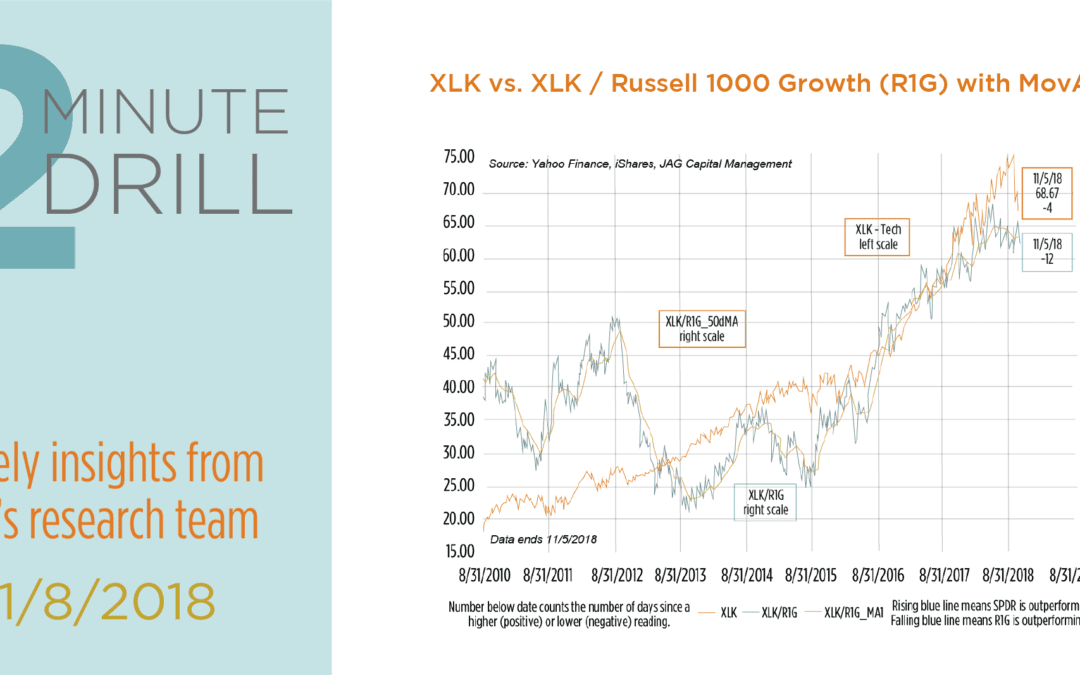

Lots of technology sector stocks have taken it on the chin during the recent market volatility. The Technology Sector SPDR (XLK) has declined almost 8% since 9/20/18, compared to a less than 7% pull-back for the S&P 500. But the longer-term relative strength line (rendered in blue in this chart) continues to look relatively healthy. We also see fundamental reasons to suspect that the technology sector remains an attractive hunting ground. To wit, operating margins continue to expand for tech. At 23%, the tech sector has the 2nd-best operating margins of all the sectors (Financials take first place with almost 28% operating margins). Furthermore, margins continue to expand compared to their 3-year average of less than 20%. It is certainly possible that tech sector profit margins could experience mean reversion in the future. That said, wide-moat businesses with strong growth outlooks and good pricing power are hard to bet against.

The recent correction in Technology stocks has brought the sector’s forward P/E back down to near-parity with the S&P 500. This does not yet meet our definition of “cheap” – note from the chart that tech stocks traded at a discount to the S&P 500 as recently as late 2017 – but we do think valuations are becoming more supportive of a technology stock rally. When we add in margin expansion and attractive top/bottom-line growth prospects for many technology stocks, we tend to lean bullish. We also note that a combination of recent volatility and negative news flow (Presidential tweetstorms, anyone?) has depressed investor sentiment on tech stocks over the past several weeks. Putting all the pieces together, we see the ingredients in place for more constructive price action looking forward into 2019.