The US stock market rebounded during the 2nd quarter, despite chaotic news flow highlighted by rising energy prices, a flattening Treasury yield curve, turmoil in emerging markets, President Trump’s tariff policies, and growing fears of a trade war between the US and China. The S&P 500 successfully navigated all this noise to generate a quarterly gain of roughly 3%. This left the benchmark index with a 2.7% year-to-date return, albeit still roughly 5.5% below its January peak.

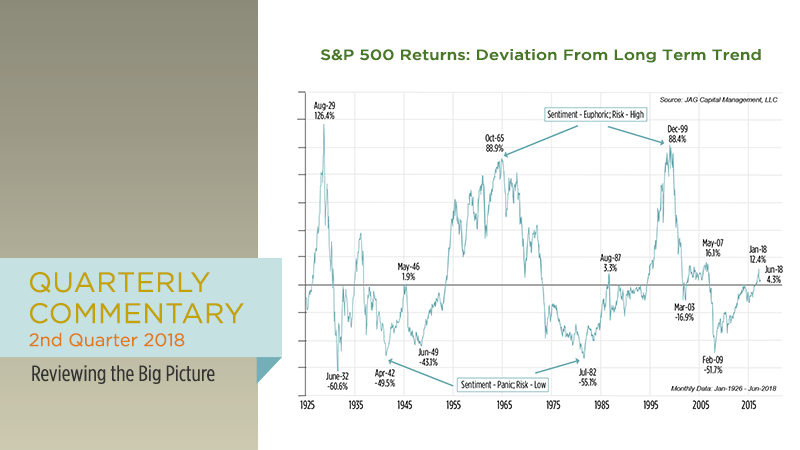

As measured by the 10-year US Treasury bond, interest rates have moved .5% higher since June 2017, leading some forecasters to proclaim that we have entered a “bear market” for bonds. We think that characterization is a bit overly dramatic. It is true that bond prices have declined modestly over the past year as a reflection of the inverse relationship between bond prices and interest rates. But so far, rates show few signs of rocketing materially higher over the coming months. In fact, we do not see a lot of fundamental reasons for bond yields to move much up or down from current levels over the next 12-18 months. Bond investors with portfolios comprised of high-quality bonds and a laddered structure of short- to intermediate-term maturities can reasonably expect relatively stable returns and cash flows. And happily, short-term fixed income instruments like money-market funds and shorter-term bonds are finally offering reasonable yields. After years of zero rates, the ability to earn even a meager return on cash equivalents should be a breath of fresh air for savers and investors.  As is usually the case, we have a generally optimistic big-picture outlook on the economy and the investment markets. Over the last several years, one has not had to look very hard to find lots of pundits who disagree with us. Most recently, we have been reading and hearing a lot of commentary that notes how “extended” the current bull market is. We find a different (and clearer) picture when we compare the inflation adjusted S&P 500 with its long-term trend since 1926. There have been three true stock market “bubbles” in the past 93 years: the 1929 mania, the Nifty 50 in the 1960’s, and the Internet bubble craziness in the late ’90’s (Remember that the 2008 Great Financial Crisis was a global liquidity collapse in the financial markets, rather than the popping of a classic bubble in stocks). Note that each of these three events occurred when the S&P 500 was trading more than 80% higher than its long-term inflation-adjusted trendline. The current reading shows that the market is only 4.3% above this trendline. Does this mean we can be certain that stocks are not on the precipice of a bear market or a big correction? No! In the short term, markets can do whatever they want to do, whenever they want to do it. However, we can say with a high degree of confidence that the stock market is not showing the signs of euphoria that it showed at past bull market “bubble” tops.

As is usually the case, we have a generally optimistic big-picture outlook on the economy and the investment markets. Over the last several years, one has not had to look very hard to find lots of pundits who disagree with us. Most recently, we have been reading and hearing a lot of commentary that notes how “extended” the current bull market is. We find a different (and clearer) picture when we compare the inflation adjusted S&P 500 with its long-term trend since 1926. There have been three true stock market “bubbles” in the past 93 years: the 1929 mania, the Nifty 50 in the 1960’s, and the Internet bubble craziness in the late ’90’s (Remember that the 2008 Great Financial Crisis was a global liquidity collapse in the financial markets, rather than the popping of a classic bubble in stocks). Note that each of these three events occurred when the S&P 500 was trading more than 80% higher than its long-term inflation-adjusted trendline. The current reading shows that the market is only 4.3% above this trendline. Does this mean we can be certain that stocks are not on the precipice of a bear market or a big correction? No! In the short term, markets can do whatever they want to do, whenever they want to do it. However, we can say with a high degree of confidence that the stock market is not showing the signs of euphoria that it showed at past bull market “bubble” tops.