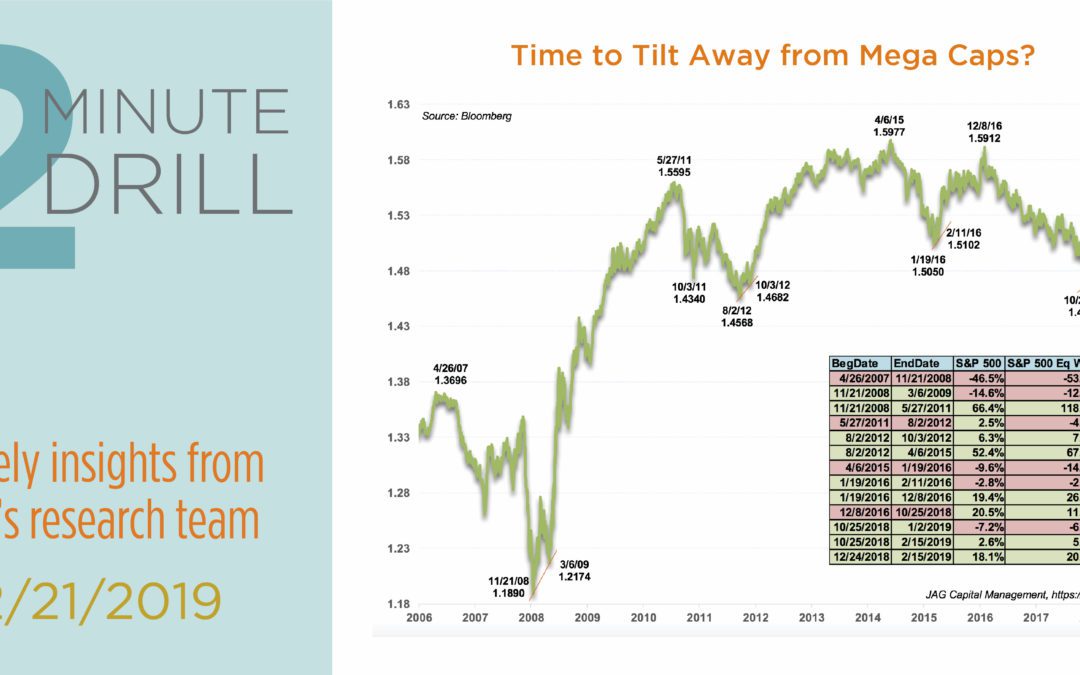

The last several years have been more than a little challenging for investors in smaller companies. Between 2014 and 2018, the small-cap Russell 2000’s annualized total return of 4.3% lagged the large-cap Russell 1000 by almost 3% per year. The difference is largely attributable to the recent dramatic outperformance by mega-cap growth stocks, sometimes collectively referred to as the “FANG” (i.e. Facebook, Apple, Netflix, Google) trade. It appears that this dynamic may be changing. As evidence, we have included this chart, which details relative performance between the traditional capitalization-weighted S&P 500 Index and the equal-weighted S&P 500.

At risk of stating the obvious, the former is dominated by the largest companies. The latter is simply an equally-weighted basket of 500 stocks, without regard to their market capitalization. When the green line is moving up, the equal-weighted S&P 500 is outperforming the cap-weighted S&P 500. When the green line is moving down, the reverse is true. Stated another way, when smaller-cap stocks are outperforming their large-cap brethren, we can expect to see the equal-weighted S&P 500 outperform the capitalization-weighted S&P 500 Index. Since the end of the financial crisis in early 2009, including the current post-12/24/18 rally, we can denote four separate inflection points in relative performance between the equal- and capitalization-weighted S&P 500. Following these instances, stocks have generally performed quite well in the subsequent 12+ month periods. But the equal-weighted S&P 500 has materially outperformed the cap-weighted index in each instance. So, while we continue to be optimistic about the intermediate-term outlook for U.S. equities, we are a bit more cautious on the biggest companies. If we are correct, it could be beneficial for stock investors to “tilt” a bit smaller in 2019.

At risk of stating the obvious, the former is dominated by the largest companies. The latter is simply an equally-weighted basket of 500 stocks, without regard to their market capitalization. When the green line is moving up, the equal-weighted S&P 500 is outperforming the cap-weighted S&P 500. When the green line is moving down, the reverse is true. Stated another way, when smaller-cap stocks are outperforming their large-cap brethren, we can expect to see the equal-weighted S&P 500 outperform the capitalization-weighted S&P 500 Index. Since the end of the financial crisis in early 2009, including the current post-12/24/18 rally, we can denote four separate inflection points in relative performance between the equal- and capitalization-weighted S&P 500. Following these instances, stocks have generally performed quite well in the subsequent 12+ month periods. But the equal-weighted S&P 500 has materially outperformed the cap-weighted index in each instance. So, while we continue to be optimistic about the intermediate-term outlook for U.S. equities, we are a bit more cautious on the biggest companies. If we are correct, it could be beneficial for stock investors to “tilt” a bit smaller in 2019.